Learn How To Manage Your Money Like A Grownup

We all know that managing our money can be tough. But it doesn’t have to be! With a little bit of effort and planning, you can take control of your finances and start living a more prosperous life. In this article, we’ll give you eight tips on how to manage your money like a grownup. From creating a budget to investing in your future, these tips will help you get your financial house in order. So read on and learn how to take control of your money once and for all!

Setting up a budget

Budgeting may seem like a daunting task, but it doesn’t have to be! By following a few simple steps, you can easily create a budget that works for you.

1. Determine your income and expenses. The first step to creating a budget is to figure out how much money you have coming in and going out each month. Track your spending for a month or two to get an accurate picture of your expenses.

2. Set financial goals. What do you want to achieve with your budget? Do you want to save up for a down payment on a house? Pay off debt? Build up your emergency fund? Whatever your goals are, make sure they are specific and measurable.

3. Make adjustments as needed. Your budget is not set in stone! As your income or expenses change, so should your budget. Be flexible and willing to make changes as needed to ensure that your budget is always working for you.

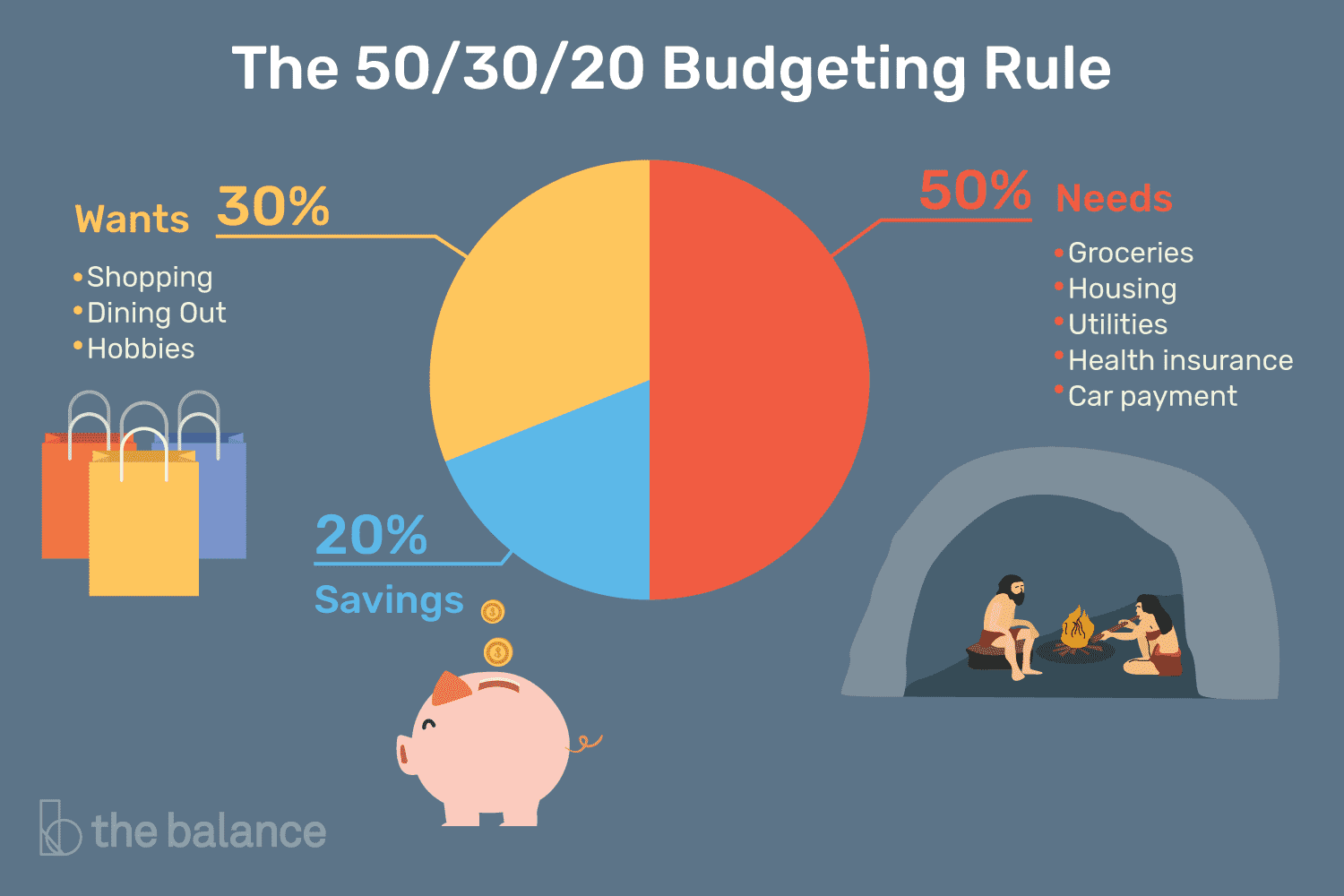

The 50/20/30 rule

If you want to get a handle on your finances, there’s no better place to start than with the 50/20/30 rule. This simple guideline can help you budget your money and make sure that you’re spending wisely.

Here’s how it works:

50% of your income should go towards essential expenses like housing, food, transportation, and utilities.

20% should be saved for future goals, such as retirement or a rainy day fund.

30% is for discretionary spending on things like entertainment, clothes, and dining out.

Of course, this is just a general guideline and your specific circumstances may require a different breakdown. But following the 50/20/30 rule can help you get a good sense of where your money should be going each month.

Why you need an emergency fund

When it comes to money, it’s important to have a plan and be prepared for the unexpected. An emergency fund is a key part of financial planning that can help you cover unexpected costs in the event of a job loss, medical emergency, or other unplanned expense.

There are many reasons to have an emergency fund, but one of the most important is to avoid going into debt. If you don’t have savings to cover an unexpected cost, you may be forced to put the expense on a credit card. This can lead to high interest charges and put you in a difficult financial situation.

An emergency fund can also give you peace of mind knowing that you have a cushion to fall back on if something goes wrong. It’s one less thing to worry about in an already stressful situation.

If you don’t have an emergency fund yet, now is the time to start saving. Begin with a goal in mind and make regular contributions to your savings account. You may need to make some sacrifices in your spending in order to reach your goal, but it will be worth it when you have the peace of mind that comes with having an emergency fund.

Investing your money

There are a lot of things to think about when it comes to investing your money. You want to make sure that you are doing it in a way that is going to help you reach your financial goals. Here are a few things to consider when you are investing your money:

1. What are your goals?

Before you start investing, you need to know what your goals are. Are you trying to save for retirement? Or are you looking to grow your wealth so that you can eventually buy a home or start a business? Once you know what your goals are, you can start researching different investment options that will help you reach those goals.

2. How much risk are you comfortable with?

Another important factor to consider when investing is how much risk you are comfortable with. Some investments come with more risk than others, but they also have the potential for higher returns. If you are not comfortable with taking on a lot of risk, there are still plenty of investment options available that can give you solid returns without putting your capital at too much risk.

3. What is your timeline?

When it comes to investing, timing is everything. If you need access to your money quickly, then you will want to avoid investments that have longer lock-up periods or that are more volatile in nature. However, if you have a longer time horizon, then these types of investments can be ideal in helping you reach your financial goals.

Common money mistakes people make in their 20’s

One of the biggest mistakes people make in their 20’s is not saving enough money. It’s important to start saving early on so you have a cushion for unexpected expenses and retirement.

Another mistake people make is not investing in themselves. This includes things like not contributing to a 401k or IRA, not taking advantage of employer matching programs, and not taking courses or learning about financial planning.

People also tend to underestimate how much debt they will have in their 20’s. This includes student loans, credit card debt, and car loans. It’s important to be aware of the interest rates on these debts and to create a plan to pay them off as quickly as possible.

Finally, many people spend too much money in their 20’s on unnecessary things like expensive clothes, nights out, and gadgets. While it’s okay to splurge occasionally, it’s important to remember that your money needs to last you through your 30’s and 40’s as well.

Final Thoughts

Managing your money can be tough, but it’s definitely worth it in the long run. Hopefully this article has given you some insight into how to get started. Remember, there’s no one-size-fits-all solution — figure out what works best for you and stick with it. And if you ever need help, don’t hesitate to ask a financial advisor.